Key message: CBAM is not yet a direct tax on most raw agricultural exports, but it is already reshaping the cost, data and competitiveness environment around Arab agri-food value chains through fertilizers, energy use, carbon accounting and EU buyer due diligence.

Executive Summary

The EU Carbon Border Adjustment Mechanism (CBAM) entered its definitive regime on 1 January 2026 after a 2023-2025 transitional reporting phase. The first covered sectors are cement, iron and steel, aluminium, fertilizers, electricity and hydrogen. Although most raw agricultural products are not directly covered today, Arab agriculture is already exposed through fertilizers, energy-intensive production, cold chains, food processing and EU buyer requirements for verified carbon data.

The agricultural relevance is strongest through fertilizers. Fertilizers are already within the CBAM scope, ammonia production is emissions-intensive, and EU fertilizer imports are linked to suppliers such as Egypt and Algeria. This means that CBAM can affect Arab agriculture both directly, through fertilizer exports to Europe, and indirectly, through input costs and carbon-documentation pressure across agri-food value chains.

Arab countries face different levels of exposure. Egypt and Algeria are especially important because of fertilizer and other CBAM-covered exports. Tunisia, Morocco and several GCC economies are exposed through fertilizers, cement, steel, aluminium, energy-intensive industries and close EU trade links. For exporters, the core risk is not only a future carbon cost; it is the possibility of losing market confidence if they cannot provide reliable emissions data. Therefore, CBAM should be treated as an early warning system for Arab agricultural exports. Export readiness will increasingly depend on carbon readiness: measuring emissions, verifying data, reducing energy and fertilizer intensity, and negotiating technical and financial support before climate-linked trade rules expand further.

Table 1. Why CBAM matters for Arab agricultural exports

| CBAM feature | 2026 change | Agricultural relevance |

| Definitive regime | Importers of covered goods must declare embedded emissions and surrender CBAM certificates. | Exporters need reliable emissions data to support EU buyers and avoid default values. |

| Fertilizers in scope | Fertilizers are among the first covered products. | Creates direct exposure for fertilizer exporters and indirect exposure for fertilizer-dependent food production. |

| EU ETS-linked pricing | Certificate prices follow EU carbon-price signals. | Low-carbon production becomes a competitiveness advantage. |

| Carbon price deduction | Carbon costs already paid in the origin country can be deducted. | Domestic carbon-pricing/MRV systems can reduce exposure. |

| Potential spillover | Climate-linked trade rules may widen over time. | Agriculture should prepare before direct inclusion. |

Sources: European Commission; Economic Research Forum; Carbon Trust; World Bank.

1. Introduction: carbon becomes a trade variable

CBAM is one of the clearest examples of climate policy becoming trade policy. It is designed to price the embedded emissions of carbon-intensive goods entering the EU and prevent carbon leakage. In practice, it also creates a new compliance infrastructure around emissions measurement, verification, certificates and buyer due diligence.

For Arab countries, this arrives at a sensitive moment, geopolitically and economically. The region is trying to expand food exports and diversify economies while facing water scarcity, heat stress, fertilizer exposure, high energy intensity and rising pressure to mobilize climate finance. Previous CEDARE insight work has already highlighted that climate policy is increasingly linked to finance, carbon markets and geopolitical uncertainty. CBAM sits directly at this intersection.

The fact that most food products are not currently in the CBAM list should not create complacency. Agriculture depends on covered or high-emission inputs, especially fertilizers and energy. Therefore, carbon performance is likely to become part of the competitiveness equation for dates, citrus, olive oil, vegetables and processed foods exported to the EU.

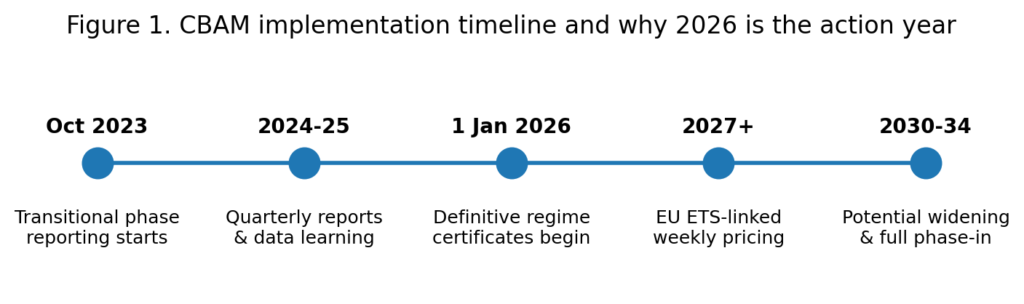

Figure 1. CBAM implementation timeline and why 2026 is the action year.

2. What changed in 2026?

During the transitional phase, CBAM mainly required reporting. From 2026, EU importers of covered goods above the relevant threshold must become authorized CBAM declarants, declare embedded emissions and surrender certificates. The price of certificates is linked to EU ETS allowance prices, making the exposure dynamic and sensitive to EU carbon-market conditions.

The first scope covers cement, iron and steel, aluminium, fertilizers, electricity and hydrogen. Fertilizers are the agricultural bridge. Nitrogen fertilizer and ammonia production are energy- and emissions-intensive. If producers cannot document actual emissions, EU buyers may rely on default values or seek suppliers with better verified data.

The result is a shift in bargaining power. Exporters with credible emissions data and lower-carbon production can defend market access and possibly gain a premium. Exporters without data may be treated as higher risk even if their real emissions are not unusually high.

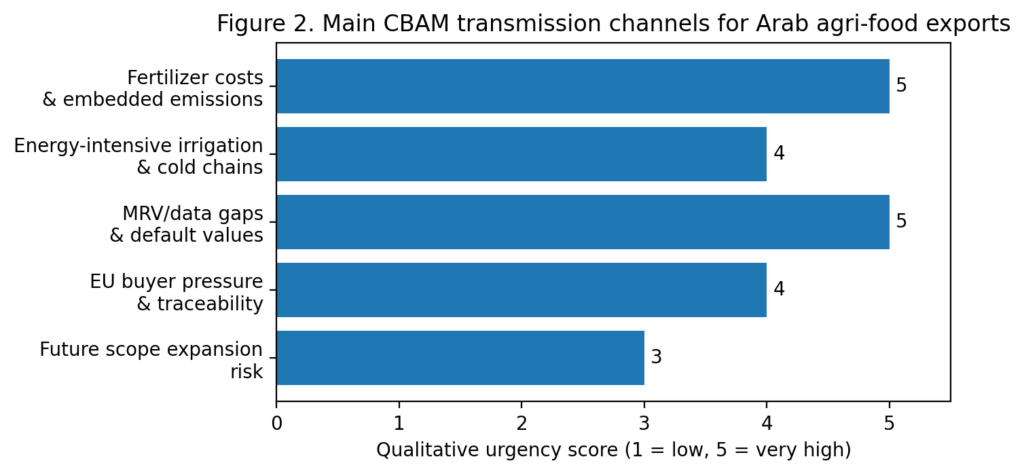

3. How CBAM reaches agriculture

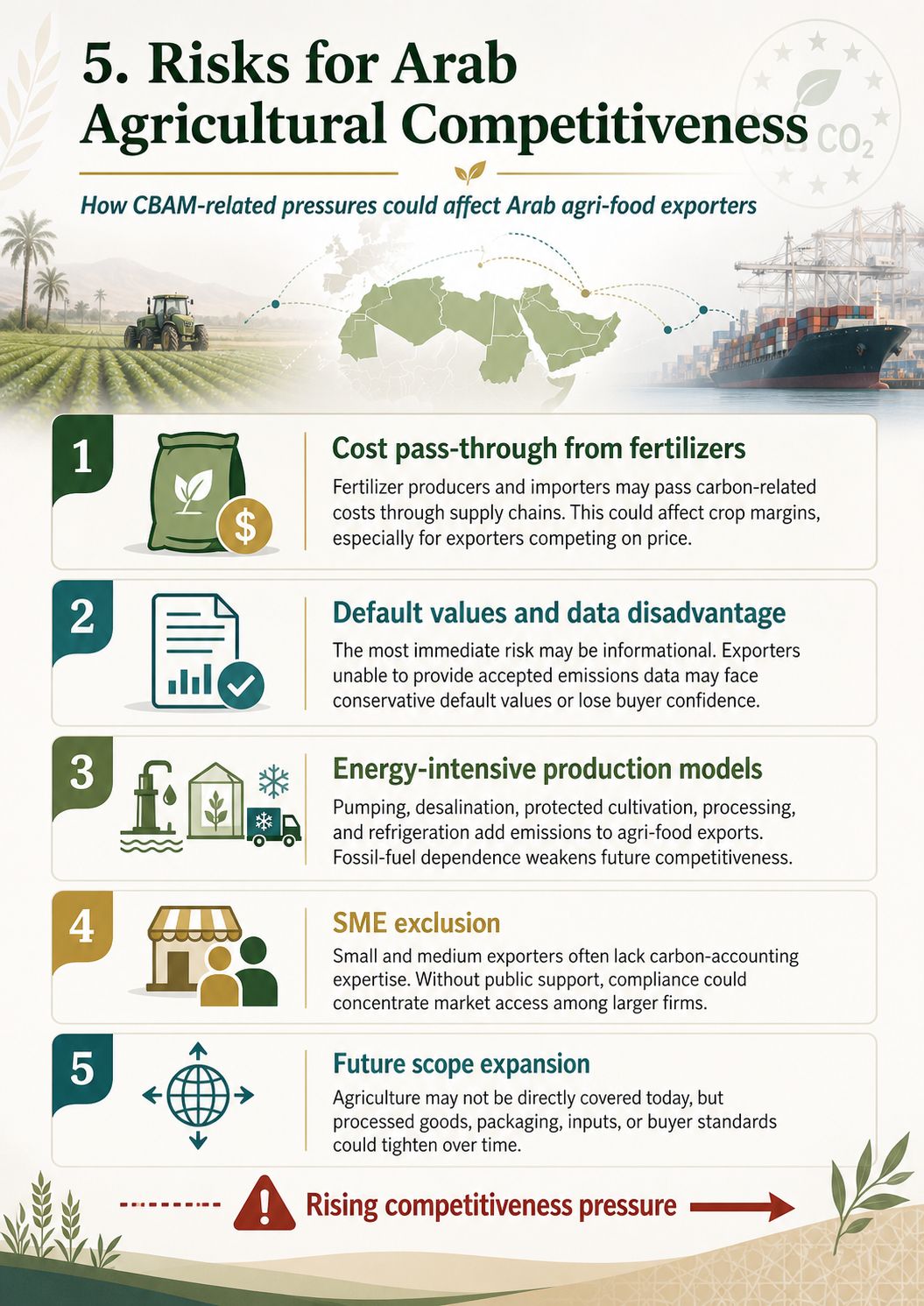

CBAM reaches agriculture through five transmission channels:

- Fertilizer cost and fertilizer carbon intensity

- Energy use in irrigation, desalination, greenhouses, processing, cold storage and refrigerated logistics

- MRV capacity: exporters need data systems, not only sustainability narratives

- Buyer pressure, as EU importers and retailers increasingly seek traceability and product carbon information

- Regulatory spillover, because climate-linked trade instruments may expand to more downstream or processed goods

These channels mean that the agricultural risk is indirect but urgent. Waiting until food products are formally covered would be a strategic mistake. By then, buyer expectations, data systems and supply-chain preferences may already have shifted.

Figure 2. Main CBAM transmission channels for Arab agri-food exports. Scores are qualitative and used for policy prioritization.

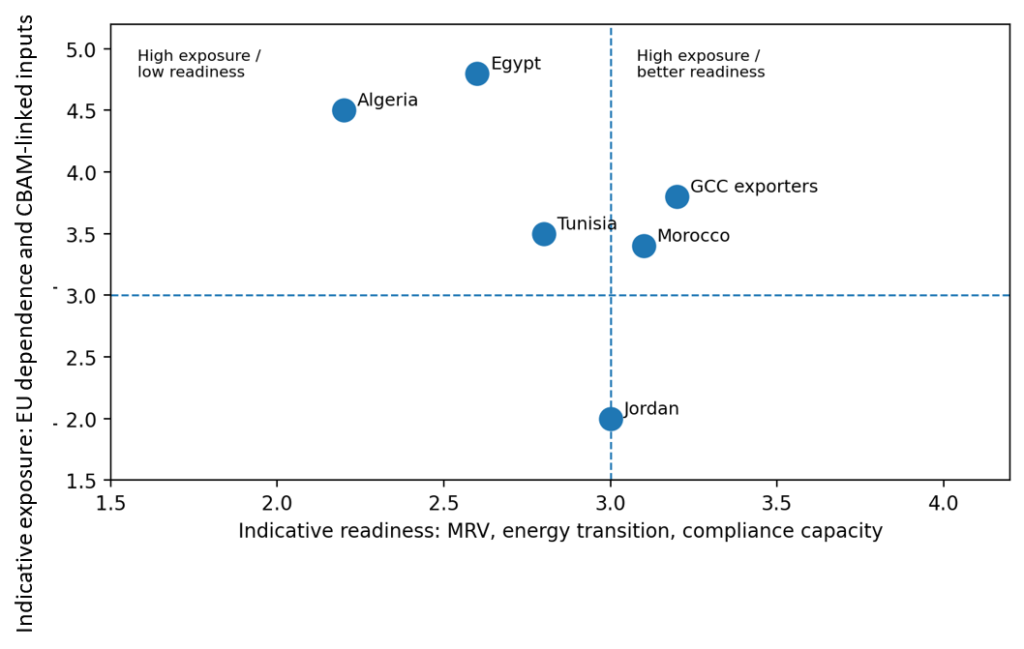

4. Arab countries most exposed to the agricultural-CBAM nexus

Exposure varies by country and value chain. Egypt and Algeria stand out because fertilizers are important in their trade relationship with the EU. Economic Research Forum analysis notes that Egypt’s CBAM-covered exports to the EU were about EUR 4.6 billion in 2022, around 10% of its total exports, and that Algeria and Egypt are among the fertilizer exporters relevant to the EU market. The Carbon Trust also reports that EU-27 fertilizer imports in 2022 were about 7.5 million tonnes, predominantly from Egypt, Algeria and the United States.

Tunisia and Morocco are exposed through their proximity to the EU, agri-food exports and links to fertilizers, cement and industrial inputs. GCC exporters are exposed through fertilizers, aluminium, steel, chemicals and energy-intensive production systems. Jordan and smaller exporters may have lower direct exposure but still face EU buyer documentation requirements.

Table 2. Indicative Arab exposure pathways

| Country/group | Exposure pathway | Agricultural relevance | Priority response |

| Egypt | Fertilizers, steel, aluminium and EU-facing exports | High fertilizer relevance and major agri-food exports to Europe | MRV, green ammonia, renewable-powered irrigation and packing |

| Algeria | Fertilizers and energy-intensive industry | Fertilizer production links CBAM to input trade | Carbon accounting and low-carbon ammonia strategy |

| Tunisia | Fertilizers, cement and EU trade dependence | Close EU market integration and food exports | Exporter carbon-footprint support and MRV templates |

| Morocco | Fertilizer value chains, renewables and agri-food exports | Potential advantage if low-carbon production is documented | Use renewables to brand low-carbon value chains |

| GCC exporters | Fertilizers, aluminium, steel and chemicals | Ammonia/urea and petrochemical links influence input markets | Scale green hydrogen/ammonia and verification |

| Jordan/others | Lower direct exposure but growing compliance needs | Niche exports face buyer documentation requirements | Shared regional tools and labs |

Figure 3. Qualitative exposure-readiness map for selected Arab exporters.

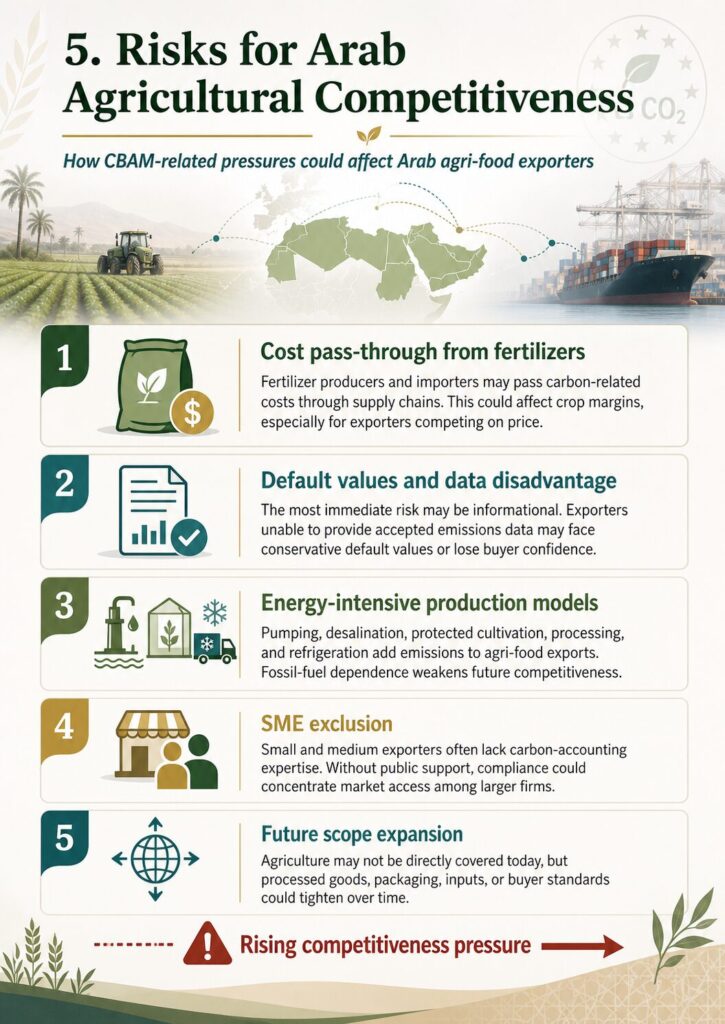

5. Risks for Arab agricultural competitiveness

6. Opportunities: from compliance to competitiveness

CBAM can also be used as a competitiveness strategy. Arab countries have strong renewable-energy potential that can reduce emissions from irrigation, desalination, cold chains and fertilizer production. Green hydrogen and green ammonia could reposition parts of the regional fertilizer industry. Digital traceability can help exporters meet buyer expectations and protect access to premium EU markets.

Carbon-market and MRV institutions are also relevant. Previous CEDARE analysis on carbon markets and COP30 stressed that global climate discourse is moving from negotiation toward implementation. The same institutional capacities needed for credible carbon markets – baselines, monitoring, verification and transparency – are also needed for CBAM readiness.

Regional cooperation would lower costs. A shared Arab CBAM-agriculture platform could develop templates, train verifiers, support laboratories, assist SMEs and negotiate technical assistance with the EU.

Table 3. CBAM readiness actions for Arab agri-food value chains

| Timeframe | Government action | Exporter action | Expected result |

| 0-6 months | Map CBAM-linked exports, inputs and vulnerable subsectors. | Identify EU-facing products, suppliers and energy hotspots. | Clear exposure map. |

| 6-12 months | Issue MRV guidance for fertilizers, packing houses, cold stores and processors. | Start facility-level emissions measurement and supplier data collection. | Lower default-value risk. |

| 12-24 months | Finance renewables for irrigation, cooling, desalination and fertilizer plants. | Invest in efficiency, solar cooling and fertilizer-use optimization. | Lower embedded emissions. |

| 24+ months | Negotiate EU support and recognition; align carbon-market institutions. | Pursue verification, product footprints and low-carbon branding. | Protected market access. |

7. Policy recommendations

- Establish national CBAM-agriculture task forces linking agriculture, trade, environment, industry, customs, standards bodies, fertilizer producers and exporters.

- Treat fertilizers as the first agricultural response area by improving fertilizer-use efficiency and accelerating low-carbon ammonia and fertilizer production.

- Build practical MRV systems and simple sectoral templates for exporters, especially SMEs, before EU buyers impose fragmented requirements.

- Decarbonize irrigation, desalination, packing, cold storage and logistics through renewable energy, energy efficiency and modern refrigeration.

- Negotiate EU technical assistance, finance for compliance infrastructure, verifier training and recognition of credible domestic mitigation systems.

- Create a regional Arab CBAM readiness platform to pool expertise, standardize methodologies and reduce the cost of compliance.

- Use verified low-carbon performance as a market asset for dates, citrus, olive oil, vegetables and processed foods.

8. Conclusion

CBAM is not only an industrial policy issue. For Arab agriculture, it is an early warning that carbon intensity, verified data and low-carbon inputs are becoming part of food-export competitiveness. Fertilizers, energy, cold chains and processing already connect agri-food exports to the CBAM logic.

Carbon readiness is becoming export readiness. Arab countries that act now can protect EU market access, reduce input vulnerability, attract climate finance and negotiate from a stronger position. Those that delay risk higher costs, weaker buyer confidence and a more difficult transition when climate-linked trade measures expand.

References

Carbon Trust. (2025, February 24). CBAM and fertilisers: What it means to importers and exporters to the EU. https://www.carbontrust.com/en-eu/news-and-insights/insights/cbam-and-fertilisers-what-it-means-to-importers-and-exporters-to-the-eu

CEDARE. (2025). The CBAM challenge: Implications for Arab countries and their strategic response. https://2025.cedare.org/the-cbam-challenge-implications-for-arab-countries-and-their-strategic-response/

Economic Research Forum. (2024, September 10). EU climate policy: Potential effects on the exports of Arab countries. https://theforum.erf.org.eg/2024/09/10/eu-climate-policy-potential-effects-on-the-exports-of-arab-countries/

European Commission. (2026). Carbon Border Adjustment Mechanism. Taxation and Customs Union. https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en

World Bank. (2025, July 2). How developing countries can measure exposure to the EU’s carbon border adjustment mechanism. https://blogs.worldbank.org/en/trade/how-developing-countries-can-measure-exposure-eus-carbon-border-adjustment-mechanism

World Bank. (2023). CBAM Exposure Indexes. https://www.worldbank.org/en/data/interactive/2023/06/15/relative-cbam-exposure-index