Executive Summary

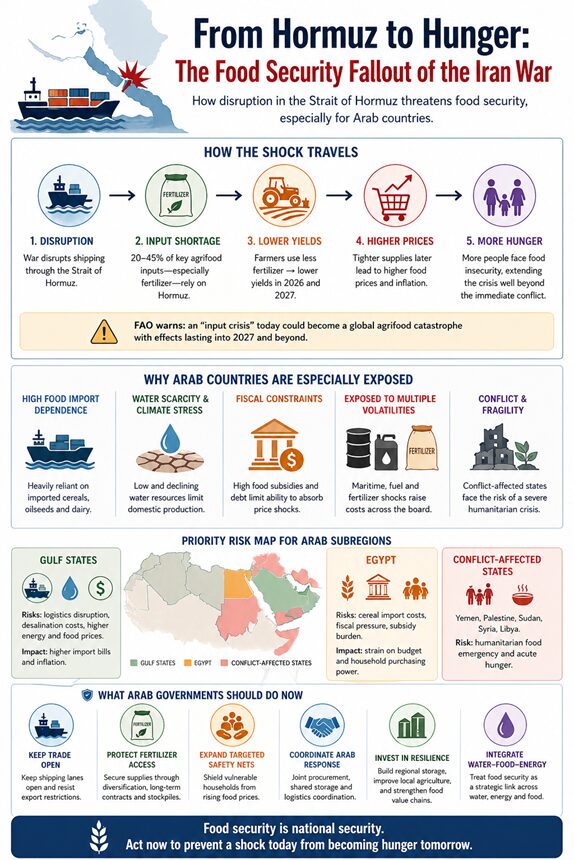

The Iran war has turned the Strait of Hormuz into a food-security chokepoint. FAO warns that 20–45 percent of key agrifood inputs depend on passage through Hormuz and that a prolonged disruption could trigger a global agrifood catastrophe, especially by constraining fertilizer access, raising energy costs, and pushing up food prices later in 2026 and into 2027. The World Bank similarly warns that the Middle East conflict is already disrupting oil and fertilizer flows, with urea prices up nearly 46 percent month on month between February and March 2026, while the World Food Programme estimates that 45 million additional people could be pushed into acute hunger by mid-2026.

For Arab countries, the shock is especially dangerous because many are structurally food-import dependent, water-scarce, fiscally constrained, and exposed to maritime, fuel, and fertilizer volatility. The most acute risks differ across the region: Gulf states face logistics, desalination, and price risks; Egypt faces cereal import and fiscal-subsidy pressure; and conflict-affected states such as Yemen, Palestine, Sudan, Syria, and Libya face the possibility of a humanitarian food emergency. The central policy implication is that Arab governments should treat food security as an integrated strategic issue linking shipping, energy, fertilizer, water, trade, and social protection rather than as a narrow agricultural question. Immediate priorities are to keep trade open, protect fertilizer access, expand targeted safety nets, coordinate Arab emergency procurement and logistics, and accelerate investment in regional storage, resilient agriculture, and water-food-energy security.

🔗 Read the full report through the link below:

Analysis

1. Why the Iran war translates into a food crisis

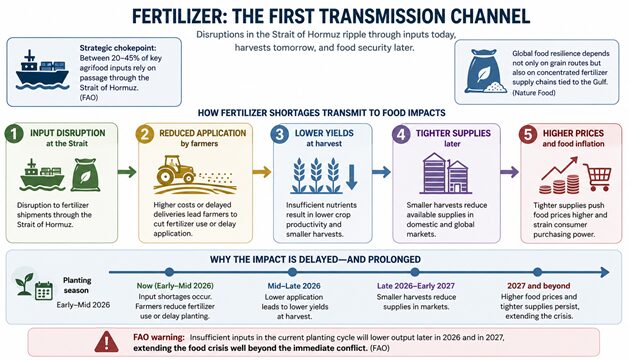

The first transmission channel is fertilizer. FAO states that between 20 and 45 percent of key agrifood inputs rely on passage through the Strait of Hormuz, and Nature Food argues that global food resilience depends not only on grain routes but also on concentrated fertilizer supply chains tied to the Gulf. This matters because fertilizer shortages do not immediately empty shelves; they first reduce application rates, then reduce yields, and only later produce higher food prices and tighter supplies. FAO therefore warns that insufficient inputs in the current planting cycle would lower output later in 2026 and in 2027, extending the crisis well beyond the immediate conflict.

The second transmission channel is energy. Fertilizer production is highly energy-intensive, especially for ammonia and urea. The World Bank reports that urea prices surged by nearly 46 percent between February and March 2026 as the conflict disrupted oil and fertilizer flows through Hormuz. Higher fuel prices also raise farm operating costs, food processing costs, road transport expenses, refrigeration costs, and maritime freight charges. This creates a broad inflationary spillover that affects importers even when physical shortages are temporarily avoided.

The third transmission channel is policy contagion. FAO explicitly urges governments to avoid export restrictions on energy and fertilizers and to reconsider biofuel mandates, since such responses worsened earlier food-price crises by insulating domestic markets at the expense of global supply. The danger is already visible in export-management behavior elsewhere. Reuters reporting indicates that China has tightened fertilizer exports to protect its domestic market, adding a second layer of scarcity to a market already squeezed by Gulf disruption. In other words, the longer the war continues, the greater the risk that a shipping shock becomes a global policy-induced food shock.

2. Why Arab countries are especially exposed

Arab countries enter this crisis from a structurally vulnerable position. UNCTAD finds that Arab countries rely heavily on food imports—especially cereals, oilseeds, and dairy products—and that in most Arab economies the share of food imports in merchandise trade exceeds the global average. It also shows that all Arab countries except Morocco were net agrifood importers during 2020–2022. This means that external price spikes and logistics disruptions transmit rapidly into domestic food systems.

The exposure is not uniform. Egypt is the region’s largest cereal importer, and UNCTAD identifies it as one of the largest cereal importers in the world. That leaves Cairo highly exposed to higher import bills, shipping costs, and subsidy pressures precisely when household purchasing power is already fragile. Yemen is even more vulnerable: UNCTAD notes that food imports exceed 31 percent of Yemen’s merchandise trade, a sign of deep structural dependence in a country already suffering conflict and humanitarian stress. Conflict-affected settings such as Palestine, Sudan, Syria, Libya, and parts of Lebanon also face a compounded risk, because international price shocks interact with damaged infrastructure, currency weakness, displacement, and aid shortfalls.

The Gulf states face a somewhat different profile of vulnerability. Their fiscal capacity offers some protection against outright shortage, but wealth does not eliminate strategic exposure. A large share of grain and food imports into the Gulf moves through or near Hormuz, and smaller Gulf countries have fewer alternative import routes than Saudi Arabia or the UAE. Moreover, Gulf food security is deeply tied to desalinated water and energy infrastructure. AP reports that more than 90 percent of desalinated water in the region depends on only 56 plants, creating a dangerous water-food-energy nexus: if conflict damages power or desalination infrastructure, food supply chains, drinking water, and domestic stability can all come under simultaneous pressure.

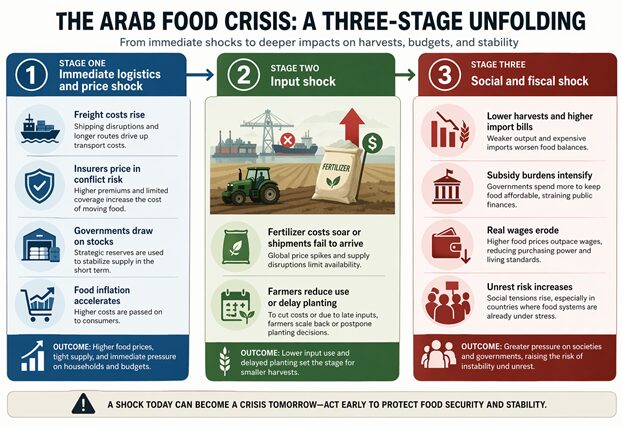

The Arab food crisis is likely to unfold in three stages:

- Stage one is an immediate logistics and price shock: freight costs rise, insurers price in conflict risk, governments draw on stocks, and food inflation accelerates.

- Stage two is an input shock: farmers in import-dependent countries reduce fertilizer use or delay planting because costs become prohibitive or shipments fail to arrive on time.

- Stage three is a social and fiscal shock: lower harvests and higher import bills intensify subsidy burdens, erode real wages, and increase the likelihood of unrest, especially where food systems are already under stress.

This sequencing is important for Arab policymakers because the most serious consequences may arrive after the immediate military headlines fade. If governments focus only on emergency stock releases without securing fertilizer flows and financing for the next planting season, they may manage the first phase of the crisis while allowing the second phase to deepen. FAO’s call for anticipatory financing is therefore highly relevant for Arab states that depend on imported inputs or on re-export and logistics hubs in the Gulf.

3. Priority risk map for Arab subregions

| Arab country group | Main vulnerabilities | Most urgent policy need |

| Gulf states | Import-route disruption, fertilizer and fuel volatility, desalination and power vulnerability, trans-shipment risk | Secure maritime corridors, protect desalination and storage infrastructure, diversify ports and suppliers |

| Egypt, Jordan, Tunisia, Morocco | High cereal and input import bills, food inflation, subsidy and foreign-exchange pressure | Expand targeted subsidies and safety nets, secure grain and fertilizer finance, diversify sourcing |

| Yemen, Palestine, Sudan, Syria, Libya | Humanitarian fragility, conflict, damaged logistics, aid dependency, currency weakness | Scale emergency food assistance, humanitarian corridors, concessional finance, and rapid import facilitation |

| Regional institutions | Fragmented procurement, weak coordination, uneven stocks and market information | Create Arab emergency coordination on food, fertilizer, shipping, and strategic reserves |

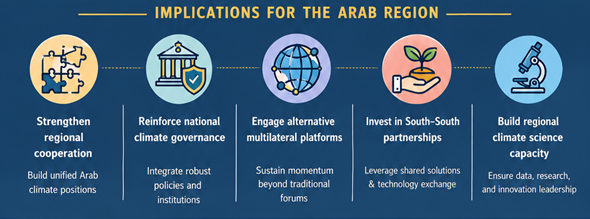

Conclusion and Policy Recommendations

The emerging food crisis under the Iran war should be understood as a compound systems shock. It begins with maritime disruption and energy volatility, spreads through fertilizer and farm-input markets, and ends in higher food prices, lower yields, fiscal stress, and potentially social instability. Arab countries are among the most exposed because many depend heavily on imported food while simultaneously facing water scarcity, climate stress, and, in several cases, active conflict. The lesson is clear: food security in the Arab region can no longer be managed only through import purchasing and emergency subsidies. It must be treated as a strategic resilience agenda that integrates shipping security, fertilizer access, water infrastructure, regional trade, and social protection.

The key policy recommendations therefore include:

- Keep trade open and resist export restrictions

- Arab governments should collectively advocate against global restrictions on fertilizers, energy, and food commodities while avoiding similar restrictions at home except in carefully targeted and temporary form.

- Secure fertilizer access immediately

- Countries should prioritize fertilizer procurement and financing now, before missed planting windows translate into lower harvests. The FAO proposal to use multilateral balance-of-payments and food-shock facilities for input financing deserves urgent Arab support.

- Build an Arab emergency procurement and logistics mechanism

- A practical regional platform could coordinate shipping intelligence, pooled purchasing, strategic reserves, and emergency rerouting through alternative ports and corridors.

- Protect the poor through targeted safety nets rather than universal price distortions

- Cash transfers, bread subsidies for vulnerable households, school feeding, and nutrition support should be scaled up quickly where food inflation is rising.

- Shield water and desalination systems as food-security infrastructure

- In Gulf countries, desalination plants, power systems, cold chains, and storage facilities should be treated as critical civilian infrastructure requiring contingency planning and protection.

- Diversify import origins and strengthen intra-Arab supply chains

- North African and Mashreq producers can play a larger role in regional agrifood trade if customs, standards, and logistics barriers are reduced.

- Invest beyond the crisis

- The medium-term agenda should include climate-resilient agriculture, strategic grain and fertilizer storage, irrigation efficiency, reduction of food loss and waste, and better market data for early warning and coordinated response.

References

- AP (2026, March). Reporting on desalination vulnerability in the Gulf.

- ESCWA, & FAO (n.d.). Arab horizon 2030: Prospects for enhancing food security in the Arab region.

- FAO (2026, March). Global agrifood implications of the 2026 conflict in the Middle East.

- FAO (2026, April 13). Protracted Strait of Hormuz crisis could turn into global agrifood catastrophe.

- Nature Food (2026, April 17). Global food security rests on the Strait of Hormuz.

- Reuters. (2026, March). Reporting on China fertilizer export curbs.

- UNCTAD (2025). Building sustainable food supply chains through trade policy in Western Asia and Northern Africa.

- World Bank (2026, March). Food security update.