1. Analytical bird’s eye view

This report assesses progress towards the developed-country commitment to mobilize jointly USD 100 billion per year since 2020. Its analytical value is not only the headline finance number; it also clarifies three dimensions that matter for Arab countries: the quantity of finance, the extent to which it addresses developing-country needs, and whether finance is linked to meaningful climate action and transparent implementation. It also looks forward to lessons for the New Collective Quantified Goal (NCQG).

The central message is mixed. According to the OECD methodology, climate finance provided and mobilized by developed countries reached USD 132.8 billion in 2023 and USD 136.7 billion in 2024, indicating that the USD 100 billion threshold was exceeded for a third consecutive year. However, this does not settle the political debate: the report emphasizes that different methodologies produce different interpretations, especially concerning loans, grant equivalents, export credits, and mobilized private finance. For Arab countries, the practical issue is therefore not whether the aggregate figure was crossed, but whether finance is accessible, concessional, predictable, aligned with national priorities, and supportive of adaptation and resilience.

2. Key findings relevant to Arab countries

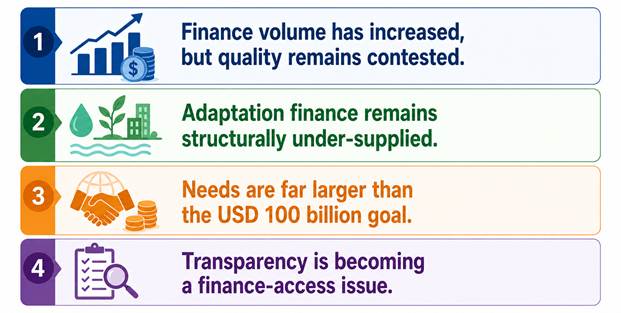

- Finance volume has increased, but quality remains contested. The growth in total climate finance is encouraging, but public finance still dominates, and the use of face-value loan accounting can overstate the real fiscal benefit for recipient countries. In assessing climate finance, OECD estimates use cash values, while Oxfam applies a net-assistance approach that discounts loans and excludes mobilized private finance. This methodological divide is highly relevant for Arab countries with constrained fiscal space or debt exposure.

- Adaptation finance remains structurally persistently limited. Adaptation-only finance averaged around USD 34.2 billion in 2023-24 under the OECD estimate, while mitigation remained the majority share of climate finance. Arab countries face acute adaptation needs in water security, agriculture, coastal zones, public health, urban heat, and disaster risk. These sectors often generate fewer direct revenues than energy or transport mitigation projects, making grants and concessional finance essential.

- Needs are far larger than the USD 100 billion goal. Thirty-three Parties in the 2025 NDC synthesis identified costed needs of around USD 1.97 trillion, while 37 developing countries in BTRs reported finance needs of about USD 3.396 trillion before 2030. The USD 100 billion goal was never designed to cover total needs, but it remains a benchmark for trust and for assessing whether finance flows respond to developing-country priorities.

- Transparency is becoming a finance-access issue. The transition to Biennial Transparency Reports (BTRs) improves clarity on finance provided, mobilized, needed and received, but developing countries continue to face capacity constraints, inconsistent reporting timeframes, and limited systems for tracking finance received. Arab countries that improve climate finance tracking, tagging and project-level reporting can strengthen both negotiation positions and access to funds.

3. How Arab countries can benefit

- Use the climate finance reporting gaps to strengthen claims for adaptation and concessional finance. Arab negotiators can use evidence on the mismatch between developing-country needs and finance characteristics to advocate for more grants, highly concessional loans, direct access, and simplified procedures, particularly for water, agriculture, coastal resilience, health and loss-and-damage-related preparedness.

- Translate NDCs, NAPs and BTRs into finance-ready pipelines. Many Arab countries have strong policy commitments but uneven project preparation capacity. Climate finance increasingly follows well-articulated needs and transparent reporting. Arab countries can benefit by converting NDC/NAP priorities into bankable programmes with costed components, results indicators, safeguards, and clear implementation entities.

- Aggregate regional projects to overcome scale and risk barriers. Several Arab adaptation needs are transboundary or regional: water scarcity, food security, drought monitoring, climate information services, coastal protection, and renewable-energy grid integration. Regional aggregation can reduce transaction costs, improve risk sharing, and attract multilateral, bilateral and private investors.

- Position adaptation-mitigation co-benefit projects as high-priority investments. Nature-based solutions, resilient irrigation, solar-powered water systems, waste-to-energy, mangrove and coastal restoration, and climate-resilient urban infrastructure can meet both adaptation and mitigation objectives, improving eligibility across climate finance windows.

4. Practical entry points for Arab countries

| Area | How to benefit | How to contribute |

| Adaptation and resilience | Prioritize grant/concessional proposals for WEFE Nexus, Nature-based Solutions, coastal zones, and health. | Share regional risk data, fund readiness support, and co-finance regional adaptation platforms. |

| Mitigation and transition | Attract finance for renewables, grids, energy efficiency, green industry, methane and transport. | Use Arab sovereign funds, national development banks and guarantees to mobilize private capital. |

| Transparency and reporting | Improve BTRs, climate budget tagging, finance received tracking and results reporting. | Create regional MRV communities of practice and common templates for project finance data. |

| Access and instruments | Use direct access entities, GCF/GEF/AF pipelines, debt-climate tools and blended finance. | Support (capacity building) Arab climate finance facilities, south-south cooperation, and contributions to multilateral funds. |

5. How Arab countries can contribute to the climate finance agenda

Arab countries are not a homogeneous group. Some are least developed or conflict-affected and should primarily seek grant-based and highly concessional support. Others are middle-income countries with significant project pipelines but limited fiscal space. GCC countries and Arab financial institutions can contribute more actively as providers, co-financiers and market shapers. This diversity can be an advantage if coordinated regionally.

Conclusion

For Arab countries, the UNFCCC Finance reporting should be read as both an accountability instrument and a strategic opportunity. It shows that aggregate climate finance has increased, but that alignment with developing-country needs remains incomplete, particularly for adaptation, concessionality, access, and transparency. Arab countries can benefit by strengthening evidence-based finance needs, preparing regional and national pipelines, and linking transparency systems to investment planning. They can contribute by mobilizing Arab public and private finance, building regional data systems, and shaping the NCQG implementation agenda so that future finance is not only larger, but also more accessible, equitable and responsive to the region’s priorities.

Selected sources used

- Standing Committee on Finance (2026) Finance reporting. https://unfccc.int/event/fortieth-standing-committee-on-finance-meeting

- Personal attendance of the Fortieth Meeting of the Standing Committee on Finance (SCF 40) in Bonn, Germany, 19-20 June 2026.